Another shock announcement was released yesterday, with self-managed superannuation rules being adjusted to prevent these structures from purchasing residential homes with debt.

Depending on where you stand and what your current financial position may be, this could feel like being robbed of another opportunity to invest — or a great opportunity to buy, as there is now one less competitor in the ring to drive up demand.

More importantly, why would the government be doing this?

And why would the banks not be pushing back against it? This is how they make money, after all.

From my humble position as a player in the game, it appears the banks may be seeking to decrease their risk exposure to residential property. If that is the case, why would they be doing this now?

Well, one may consider if interest rates continue to rise because inflation remains persistently high — which is common during times of global conflict and shortages — this will place further upward pressure on rates.

These global conflicts also commonly overlap with internal civil frustration or unrest, to put it bluntly. At present, some of this frustration is being expressed through politics as it pushes One Nation to become, if not the ruling party over time, at least a serious power player in policy decision-making.

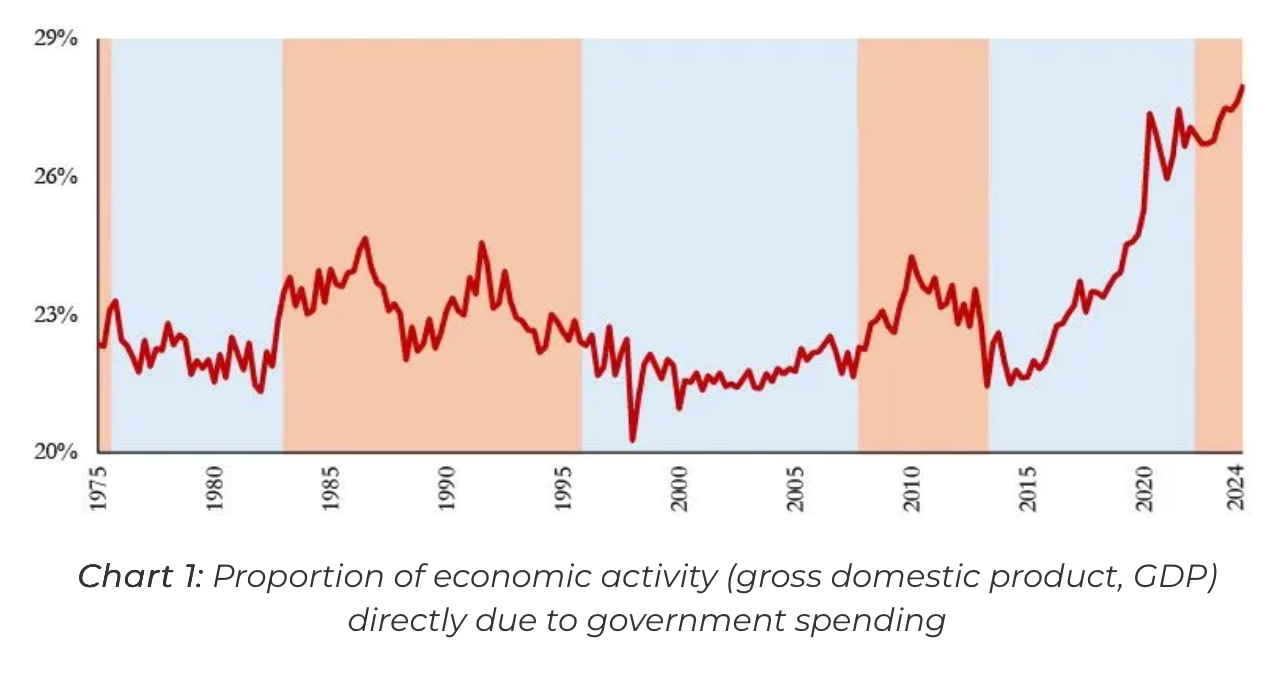

What is Pauline and One Nation’s number one policy promise? To reduce immigration, which has contributed to rapidly rising rents ever since 2021. Their second policy is to cut government spending deeply.

During normal, stable times, these policies may not lead to a serious downturn. But as we know, these are not normal times. Housing prices are very high relative to incomes, and government jobs have been one of if not the largest creators of direct and indirect employment for some time.

I’m not here to say whether this is good or bad. I’m simply suggesting that the Melbourne and Sydney markets may be in for a few more tough years — creating both dangers and opportunities — that investors should be cautious about exposure to floating-rate debt and consider commercial property more seriously - if even the banks see it as a more viable option to be exposed to.

What are your thoughts? I'd love to hear from you.