One of the biggest misconceptions in commercial property investing is that a vacant tenancy is always a bad outcome. It certainly can be. But only if you're unprepared. In commercial real estate, it's common for a new tenant to fund their own fit-out, sometimes in exchange for a rent-free period. However, I've increasingly become a fan of another approach. Rather than asking the next tenant to spend tens (or hundreds) of thousands of dollars before they can even open their doors, why not deliver a space that's almost move-in ready? The renovation concept below is a proposal I've prepared for one of our recently acquired assets if it ever becomes vacant. (Before ➡️ After) A relatively modest renovation could dramatically improve the property's appeal while reducing the time, stress and upfront capital required from the incoming tenant. From a business owner's perspective, paying 10-15% more in rent can be a worthwhile trade-off if it means: ✅ Opening weeks or months sooner ✅ Avoiding a major fit-out bill ✅ Starting to generate revenue immediately ✅ Walking into a professional, modern premises For investors, preparation changes the psychology of a vacancy. Instead of seeing an empty tenancy as something to fear, it becomes an opportunity to reposition the asset, attract a higher-quality tenant, strengthen lease terms, and potentially improve the property's long-term value. No renovation is perfect. Every project involves trade-offs, budgeting decisions and lessons along the way. But having a well-considered plan before a vacancy occurs gives you options when others are reacting under pressure. Sometimes the best value isn't found in buying a better property. It's created by seeing the potential that others overlook. 👇 Would you rather offer tenants a blank shell and lower rent, or a move-in-ready space with a slightly higher rental?

Commercial property can be an incredible way to build passive income and long-term financial independence . But here's something I've learned... The investors who achieve the best long-term outcomes don't necessarily buy the "best" properties. They usually make better decisions before they ever make an offer. If you're a busy professional or business owner considering your first commercial property, here are six questions I'd encourage you to answer first. 1️⃣ Why am I investing? Before looking at properties, define what success actually looks like . Are you trying to: Replace part of your salary? Fund your children's education? Create financial independence? Build generational wealth? Your goals will evolve over time, but writing them down gives you something to measure every future decision against. 2️⃣ What type of investor am I? Be honest about your strengths. Have you renovated properties before? Are you an experienced project manager? Or are you already time-poor because of your career or business? If you enjoy managing projects, value-add opportunities may suit you well. If your time is your most valuable asset, a quality property with a strong tenant and longer lease may provide a better fit. The best investment is often the one that matches your lifestyle , not someone else's. 3️⃣ Do I have the financial foundations? Commercial property isn't just about having a deposit. It's about having the confidence to hold the asset through changing market conditions. Ask yourself: Do I have sufficient funds for a deposit? Am I consistently saving each month? Do I have enough liquidity if something unexpected happens? While opportunities exist across many price points, stable commercial investments with quality tenants are often found from around the $600,000+ price range. Depending on your lending structure, many investors aim to have a substantial deposit and financial buffer before purchasing. 4️⃣ How well do I handle uncertainty? Every investment will experience challenges at some point. The difference is how prepared you are when they arrive. Practical strategies include: ✅ Maintaining a strong household savings rate ✅ Holding 6–12 months of property costs in reserve ✅ Having a vacancy or renovation plan before it's ever needed Equally important is mindset. Successful investors tend to see problems as opportunities to improve an asset rather than reasons to panic. 5️⃣ What am I doing today to become a better investor? Great investors don't wait until settlement to start learning. Simple habits compound over time: 📚 Read books on economics, business and investing. 🎧 Listen to quality podcasts. 🏦 Speak with commercial mortgage brokers to understand your borrowing capacity. 🏢 Talk to experienced commercial property professionals about what ownership actually involves. Knowledge reduces uncertainty—and better decisions usually follow. 6️⃣ Who is helping me think bigger? One of the fastest ways to grow is to spend time with people who have already achieved what you're working towards. They've made mistakes, solved problems and gained perspective that can save you years of learning through trial and error. A strong network doesn't just provide knowledge. It helps you stay focused on your long-term vision when markets inevitably become noisy. Final thoughts Commercial property isn't about finding a perfect investment. It's about building the right foundation before you buy. The stronger your finances, your knowledge and your strategy, the greater your ability to remain disciplined through changing market conditions. That's often what separates investors who build lasting wealth from those who continually chase the next opportunity. 💬 Which of these six questions do you think investors overlook most often? I'd love to hear your thoughts in the comments.

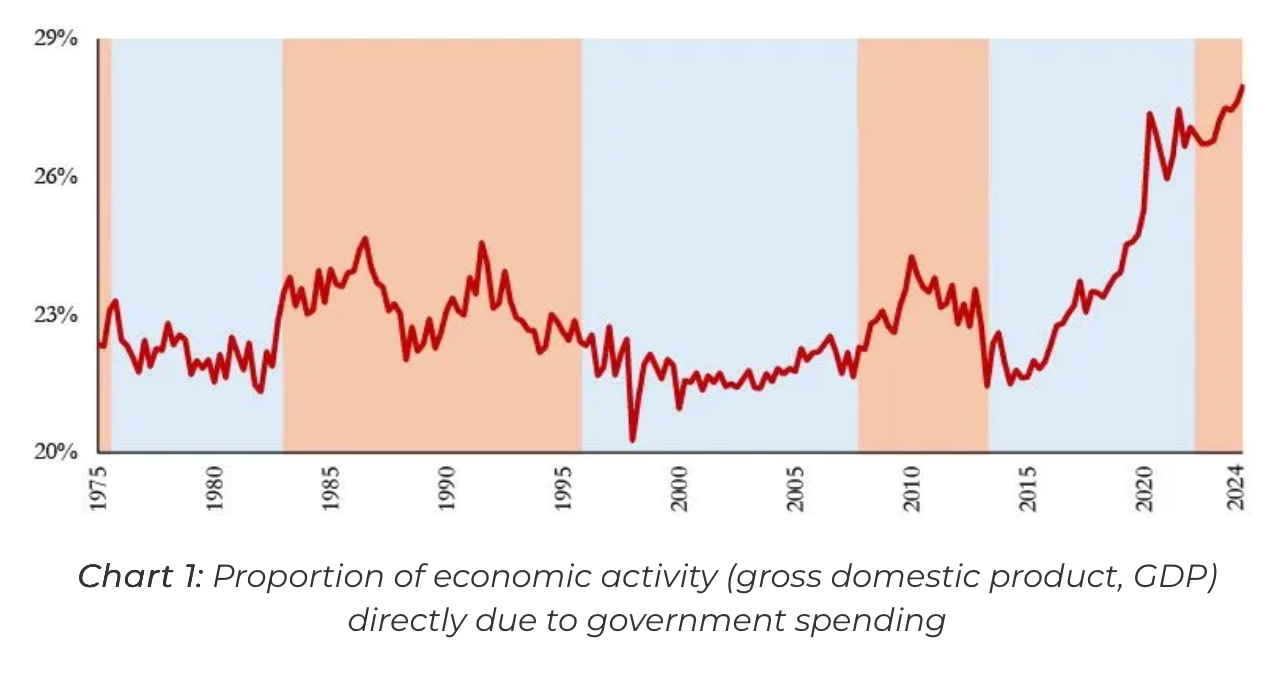

Another shock announcement was released yesterday, with self-managed superannuation rules being adjusted to prevent these structures from purchasing residential homes with debt. Depending on where you stand and what your current financial position may be, this could feel like being robbed of another opportunity to invest — or a great opportunity to buy, as there is now one less competitor in the ring to drive up demand. More importantly, why would the government be doing this? And why would the banks not be pushing back against it? This is how they make money, after all. From my humble position as a player in the game, it appears the banks may be seeking to decrease their risk exposure to residential property. If that is the case, why would they be doing this now? Well, one may consider if interest rates continue to rise because inflation remains persistently high — which is common during times of global conflict and shortages — this will place further upward pressure on rates. These global conflicts also commonly overlap with internal civil frustration or unrest, to put it bluntly. At present, some of this frustration is being expressed through politics as it pushes One Nation to become, if not the ruling party over time, at least a serious power player in policy decision-making. What is Pauline and One Nation’s number one policy promise? To reduce immigration, which has contributed to rapidly rising rents ever since 2021. Their second policy is to cut government spending deeply. During normal, stable times, these policies may not lead to a serious downturn. But as we know, these are not normal times. Housing prices are very high relative to incomes, and government jobs have been one of if not the largest creators of direct and indirect employment for some time. I’m not here to say whether this is good or bad. I’m simply suggesting that the Melbourne and Sydney markets may be in for a few more tough years — creating both dangers and opportunities — that investors should be cautious about exposure to floating-rate debt and consider commercial property more seriously - if even the banks see it as a more viable option to be exposed to. What are your thoughts? I'd love to hear from you.

Commercial property can be a powerful way to build passive income. But for many families and busy professionals, there’s one question sitting in the background: What happens if the tenant leaves? A vacancy doesn’t just mean lost rent. It can also mean: Mortgage pressure Ongoing outgoings with no income Stress on household cashflow Feeling forced to accept the wrong tenant or lower rent just to fill the space That’s why I believe the biggest mistake first-time commercial investors make is not buying the “wrong suburb” or “wrong sector”… It’s buying before their financial foundations are strong enough. Here are 4 ways to protect your family before you buy. 1️⃣ Build strong cashflow first. If your household, business or wider portfolio already produces a surplus, a vacancy becomes far less dangerous. Strong cashflow gives you breathing room, options and time to make better decisions rather than reactive ones. There are many levers available to boost cash flow that few notice, for example where appropriate: - Switching your home mortgage from principal and interest to a fixed rate interest only loan and redirect the excess income into savings. - Consider what you can rent out or sell to minimise expenses and maximise income. - Review finances and ask yourself where is my money going exactly? Is it in line with my long term objectives? 2️⃣ Keep liquidity on hand Cash, redraw capacity or liquid investments can turn a vacancy from a crisis into an inconvenience. It gives you the ability to: Cover loan repayments and outgoings Improve the property if needed Wait for the right tenant rather than taking the first one available 3️⃣ Use conservative debt The wrong debt structure can turn a good property into a stressful one. A safer approach may involve: Manageable loan repayments Fixed rates Buffers in place Structuring loans to be property specific and avoiding cross collateralisation where appropriate 4️⃣ Have a value-add plan before you need it If a tenant leaves, what’s Plan B? Could the property be: Cosmetically improved? Repurposed for another tenant type? Reconfigured to suit stronger demand? Repositioned to achieve better rent or lease terms? Having that thought through in advance can make a huge difference. My view For families and busy professionals, commercial property should feel like a step toward freedom — not a source of constant financial stress. The goal isn’t to eliminate every risk. It’s to structure your finances so that if something goes wrong, it doesn’t derail your family’s plans or your long-term passive income strategy. Commercial property can be a fantastic wealth-building tool 📈 But it works best when the asset is backed by a strong financial foundation.